The Streamlined Energy and Carbon Reporting (SECR) legislation came into effect on 1 April 2019 with wider content and affecting around 10,000 companies for the first time.

OVERVIEW

You must comply if

- You are a quoted company or a large unquoted company (see below) and

- You are over the 40,000 kWh per year exemption limit for low energy users (so typically with more than £1,000 to £6,000 annual energy spend).

If your financial year ends in April, May, June, July, August, September, October, November or December each year – your first SECR-compliant Directors’ Report is for your financial year ending in 2020.

If your financial year ends in January, February or March each year – your first SECR-compliant Directors’ Report is for your financial year ending in 2021.

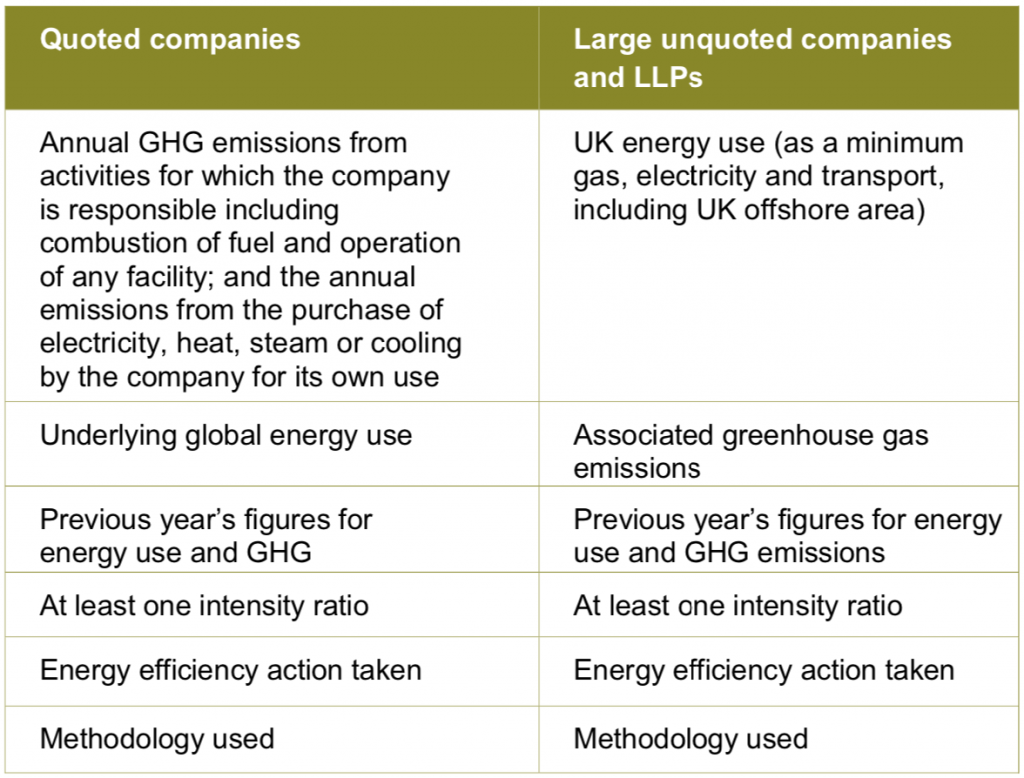

The table summarises the disclosure obligations for quoted companies and for large unquoted companies. You can omit minor energy uses and emissions up to around 2-5% of your total.

Extracts which follow are from the government’s “Environmental Reporting Guidelines: Including streamlined energy and carbon reporting guidance March 2019”.

CHAPTER AND VERSE

The Companies Act 2006 (Strategic Report and Directors’ Report) Regulations 2013 introduced changes to require quoted companies to report their annual emissions and an intensity ratio in their Directors’ Report.

The 2018 Regulations bring in additional disclosure requirements for quoted companies.

The 2018 Regulations also introduce requirements for large unquoted companies and limited liability partnerships to disclose their annual energy use and greenhouse gas emissions, and related information.

Changes … take effect from 1 April 2019, and cover financial reporting years starting on or after this date. Your reporting period should be for 12 months and should ideally correspond with your financial year.

Quoted companies … are those whose equity share capital is officially listed on the main market of the London Stock Exchange; or is officially listed in an European Economic Area State; or is admitted to dealing on either the New York Stock Exchange or NASDAQ.

The definition of “large” is the same as applies in the existing framework for annual accounts and reports, based on sections 465 and 466 of the Companies Act 2006. The qualifying conditions are met by a company or LLP in a year in which it satisfies two or more of the following requirements:

Turnover £36 million or more,

Balance sheet total £18 million or more,

Number of employees 250 or more.

The information in this Native-Hue energy management briefing should be verified before use for compliance purposes.